These are major redevelopment sites where dwellings have been constructed. It is the final stage of the redevelopment pipeline.

On this page:

Major redevelopment summary 2021

Major redevelopment sites are those which were previously used for commercial, industrial, educational or residential purposes. These sites have been identified through the planning process of being able to accommodate 10 or more dwellings. Major redevelopment sites play a significant role in how Melbourne’s growth is managed.

In 2021 there were 148,394 dwellings in the major residential redevelopment project pipeline across metropolitan Melbourne. This is less than the 162,423 dwellings in 2020.

Of these, the inner and middle ring municipalities continue to be the dominant regions accounting for 85% or 125,683 of these dwellings.

80% of these dwellings are expected to be constructed in buildings of 4 or more storeys.

In 2021 there were 19,788 dwellings completed on major redevelopment sites. More than the 15,597 dwellings completed in 2020.

The redevelopment pipeline

Redevelopment sites

At December 2021, there were 148,394 dwellings on major residential redevelopment sites that were either under construction or in the development pipeline. 80% of dwellings proposed for major redevelopment sites are expected to be built in buildings of four or more storeys.

Annual supply of major residential redevelopment site dwellings by built form

* new category in 2017

In 2021 there has been a decrease of 14,029 dwellings in the redevelopment pipeline compared to 2020. The majority of this is due to fewer projects being under construction in 2021. However, the number of dwellings in the redevelopment pipeline has been declining since 2016. This decline in the supply of dwellings corresponds in the decline in apartment approvals in the inner suburbs, particularly in the City of Melbourne, since 2017.

Some of this decline is due to projects proposed for major redevelopment sites being discontinued at various stages. Some redevelopment sites are withdrawn as residential projects and the site is repurposed for other uses such hotels, offices and other commercial purposes.

The inner and middle ring municipalities continue to be the dominant regions for the supply of anticipated dwellings on major redevelopment sites with nearly 85% of dwellings .

83% of current and anticipated major development activity in inner Melbourne are in apartment projects of ten storeys or greater. In comparison, the middle ring redevelopment projects provide a greater range of dwelling types. Apartment projects ten storeys or greater make up a third of the middle ring dwelling pipeline, while low rise projects, such as detached houses, townhouse and low scale apartment projects make up nearly 20% of the dwellings in the pipeline.

Supply of major residential redevelopment dwellings by region and built form

Across the metropolitan region, 24% (35,182) of anticipated major redevelopment activity is in the Melbourne Local Government Area (LGA) and mainly consists of apartments greater than 10 storeys. Port Phillip, where opportunities exist for larger apartment buildings, has the second highest number of anticipated dwellings followed by Maribyrnong where there are some large redevelopment sites.

The remaining Inner and Middle Ring LGAs have a mix of development types, with 4 to 9 storey developments common in most of these municipalities.

In 2021 there were 19,788 dwellings assessed as completed on major redevelopment sites, this is more than the 15,597 completed in 2020. The City of Melbourne had the highest level of dwellings in the pipeline (35,182) and completed dwellings (6,165) in 2021.

Strategic land supply policy

15 years of land supply

Clause 11.02-1S of the State Planning Policy Framework of the planning scheme identifies the need to “Plan to accommodate projected population growth over at least a 15-year period and provide clear direction on locations where growth should occur.” Redevelopment land supply is one element of the land required to provide dwellings to service population growth. Supply is also provided through greenfield land which is monitored by the Urban Development Program – Greenfield and infill development.

Unlike the location of future greenfield development, which has been identified through a range of strategic planning documents, the horizon for major redevelopment sites is shorter. Given the short-term nature of identifying major redevelopment sites, an assessment of the number of years of supply for major redevelopment sites cannot be made using site-specific information. However, monitoring of major redevelopment sites over a number of years indicates that the market identifies new opportunities.

Plan Melbourne 70:30 aspiration

Policy 2.1.2 of Plan Melbourne sets an aspirational scenario where 70% of net additional dwellings are located within established Melbourne and 30% in the growth areas. The 70:30 aspirational scenario is designed around a sustained change over a long time period. It is anticipated the share of new dwellings being built in the growth areas will decrease over time as greenfield land is consumed and development increases in the established parts of Melbourne.

Historically, the share of net additional dwellings in the established areas of Melbourne has approached 70%. Since 2016, the share of dwelling approvals occurring in the established parts of Melbourne have declined from 64% to 44% in 2021. This decline in the share of net dwelling approvals can be attributed to continued strong greenfield development. Demand for greenfield housing remained strong driven by federal and state stimulus initiatives such as Homebuilder to maintain construction and development activity during the coronavirus (COVID-19) pandemic, that enabled development to be brought forward.

Population growth prospects

Population growth is a key factor in the development of new housing. Before the coronavirus (COVID-19) pandemic, Victoria was the fastest growing state in Australia, reflecting its attractiveness as a place to live, work and study.

The population grew at an average of more than 2.0 per cent per annum for most of the previous decade. Victoria’s population decreased during the pandemic period. This was the first decrease in many years.

Victoria’s population peaked at almost 6.694 million people in June 2020. Growth was below 100,000 for the year though, compared with an average growth of 140,00 for the five previous years. During the year 2020/21 Victoria’s population decreased by 44,700 people to finish at 6.649 million in June 2021.

There is considerable uncertainty around the post-COVID future. It is unknown when Victoria will re-open for a return to ‘normal’ levels of overseas migration. There is a common assumption driving some published projections. It is assumed migration will return over two-to-three years. Recent projections produced by the Commonwealth and Victorian Governments contain similar assumptions and short-term results.

The 2022-23 State Budget projections show Victoria’s population growing by 0.1 per cent in 2021-2022 before growth increases to 1.1 per cent in 2022-2023 and 1.6 per cent over the following year as borders reopen.

The Commonwealth Budget projects that Victoria's population is projected to increase by 0.5 per cent in 2021-2022 before growth increases to 1.4 per cent in 2022-2023 and 1.8 per cent over the following year.

Current housing activity

Despite the disruption to population growth, residential development activity in Victoria remains strong.

In the 12 months to January 2022, there were about 70,000 new homes approved for construction across Victoria. About 47,000 of these approvals were for detached houses, one of the highest number of approvals ever recorded over a 12-month period.

There were also nearly 13,000 approvals for medium-density units and townhouses, and about 10,000 approvals for higher-density apartments. Most of these were located in the established parts of Melbourne.

Victoria currently leads Australia in residential building activity. During the same 12-month period New South Wales saw about 62,000 approvals and Queensland about 44,000 approvals. Much of the new housing across Victoria has been built in greenfield residential areas - both in Metropolitan Melbourne and Regional Victoria.

Method

The Urban Development Program monitors and reports on major residential redevelopment projects across metropolitan Melbourne. Data is collected through analysis of aerial imagery, planning permits, real estate websites and websites of developments.

Development within the established parts of Melbourne takes the form of minor infill development (less than 10 dwellings in a project) as well as major redevelopment sites with 10 or more dwellings in a project. The supply of minor infill, sites that produce between 1 to 9 dwellings are not monitored as part of this data collection.

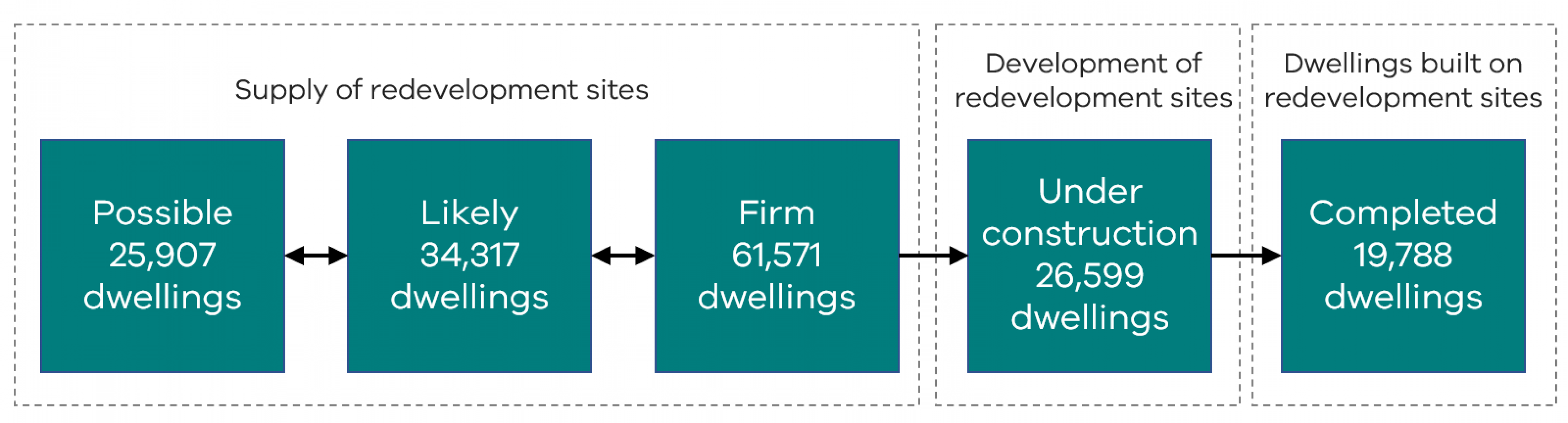

The UDP Redevelopment tracks projects as they progress through the development pipeline from the supply of sites through to finished dwellings. The pipeline is broken up into three categories of supply and 5 stages of development.

Supply of redevelopment sites stages

Possible – early indicator of the location of future major redevelopment sites. Sources include:

- DELWP

Likely – major redevelopment sites that are within the planning process. Sources include:

- LGA planning registers

- PPARS (DELWP)

- Real estate websites

Firm – major redevelopment sites that have been approved and/or taking sales enquires and registrations. Sources include:

- LGA planning registers

- PPARS (DELWP)

- cadastre (DELWP)

- websites of developments

- Real estate websites

Development of redevelopment sites

Under Construction – building works being carried out on major redevelopment sites. Sources include:

- address points (DELWP)

- cadastre (DELWP)

- aerial photography (DELWP)

Dwellings built on redevelopment sites

Completed – completed building on major redevelopment sites. Sources include:

- address points (DELWP)

- cadastre (DELWP)

- aerial photography (DELWP)

Projects within the pipeline can move between stages (forward or backward) or can be abandoned.

Get the data

Spatial data in a number of formats including ESRI shp and MapInfo TAB. You will require GIS software to use this data.

Definitions of spatial data attributes are available in the data dictionary below.

Download the data used to create the graphs shown in the report above.

Glossary

The UDP- Redevelopment tracks sites as they progress through the development pipeline from the supply of sites through to finished dwellings. Temporally, the pipeline stages are: possible, likely, firm, under construction and completed.

Established Melbourne is defined as the urban land within the Urban Growth Boundary that is not identified as growth area land (see the Urban Development Program – Greenfield for the location of greenfield land).

These are major redevelopment sites that have been approved and/or taking sales enquires and registrations. It is the third stage of the redevelopment pipeline.

These are major redevelopment sites that are within the planning process. It is the second stage of the redevelopment pipeline.

These are sites identified going through the planning systems where 10 dwellings or more have been proposed.

This is an early indicator of the location of future major redevelopment sites. It is the first stage of the redevelopment pipeline.

These are major redevelopment sites where building works are being carried out. It is the fourth stage of the redevelopment pipeline.

Page last updated: 11/06/23